Humanoid Robots Are Poised to March Into the Real World

Many predict 2025 will be a milestone year for the robotics industry — comparable to the iPhone’s debut for smartphones or ChatGPT’s launch for AI — with the mass production of humanoid robots.

This expectation stems from breakthroughs in key robotics hardware and software technologies, coupled with manufacturers’ growing readiness to scale up production.

In China, excitement about the potential of humanoid robots soared after the Lunar New Year’s Eve, when 16 of Unitree Robotics’ general-purpose robots appeared at the Spring Festival Gala. Performing a tightly choreographed Chinese folk dance alongside human dancers, the robots — dressed in traditional floral-patterned cotton jackets and spinning red handkerchiefs — wowed more than a billion viewers with their synchronized movements.

The performance marked a pivotal moment for China’s robotics and embodied intelligence sector, igniting a surge of interest and investment. According to Shenzhen-based consultancy Gaogong Industry Institute, the sector saw 27 financing deals in the first two months of 2025, totaling 4.45 billion yuan ($614 million). Caixin estimates that nearly 5 billion yuan was raised in 2024, suggesting that early 2025 funding has already neared last year’s total.

Embodied intelligence has become a buzzword in AI and investment circles in the past two years. Unlike traditional industrial robots, such as mechanical arms, embodied intelligence focuses on humanoid robots that can adaptively perceive and interact with their environments using human-like physical forms. These robots emphasize advanced motor coordination — akin to a cerebellum — and cognitive abilities in vision, language and movement, enabling more natural and versatile interactions. This shift represents a move beyond factory automation toward robots capable of more complex, human tasks.

The global excitement surrounding AI-native hardware began with the launch of OpenAI’s ChatGPT 3.5 in late 2022, which increased interest in humanoid robots. “Humanoid robots are complex and imaginative, aligning with people’s visions of the future,” said Tu Danning, an investment manager at Taihe Capital.

Since 2024, several Chinese regions have rolled out incentive policies to support AI and robotics industries as the country aims to lead the global tech race. Hangzhou in the eastern Zhejiang province offers up to 5 million yuan in rewards and 25% project funding subsidies, while Beijing has established a 100-billion-yuan government investment fund to support startups. Southern Guangdong province provides up to 50 million yuan for robotics companies and 10 million yuan for AI firms, and Shenzhen has set bold targets for embodied intelligence, aiming to cultivate more than 10 companies valued at more than 10 billion yuan and achieve an industry scale exceeding 100 billion yuan by 2027. Shanghai and the southwestern Sichuan province have also introduced supportive measures.

While China and the United States are seen as equals in AI and robotics technology, China’s strengths in large-scale manufacturing and software optimization give it an edge in industrializing humanoid robots.

“The U.S. excels in theoretical innovation, but China is unmatched in engineering software algorithms and mass production,” said Duan Bing, a tech analyst at Nomura. “Humanoid robotics perfectly combines these two strengths.”

Investment frenzy

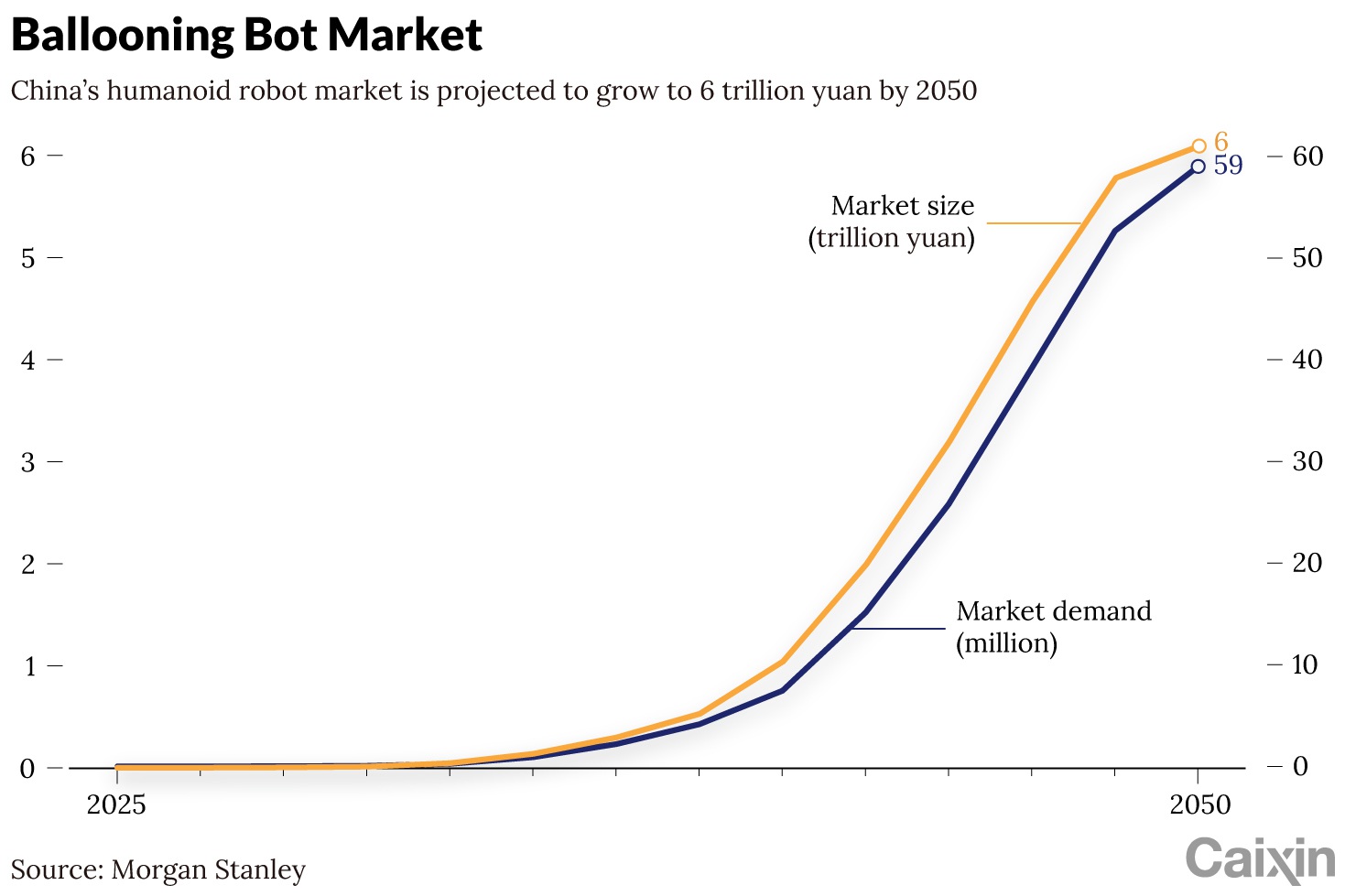

Jin Hanmin, vice president of Lighthouse Capital, predicts the humanoid robot market will become a “massive opportunity,” potentially 10 times larger than the new energy vehicle sector. “It’s foreseeable that many households will own two to three humanoid robots,” he told Caixin.

Unitree’s Chinese New Year dance performance has ignited a surge in investment interest in embodied intelligence. “Investors flooded in to discuss our projects — some couldn’t even secure a spot for roadshows, while others issued term sheets after just one meeting,” Jin said.

Liu Xin, chief executive of Soho Blink, a startup founded in July 2024 specializing in dexterous robotic hands, said the company has been approached by a number of government and private investors for possible partnership, though it has yet to sign any deal.

The sector has seen a wave of funding in recent months. On March 6, AI2 Robotics and LimX Dynamics each said they had secured several hundred million yuan in funding. In January, Fourier, a humanoid robotics developer, closed a Series E round of nearly 800 million yuan. Just a month earlier, MagicLab, founded in January 2024, raised 150 million yuan, with its robot MagicBot now training on factory production lines for tasks like inspection and material handling.

As robotics startups — some less than two years old — race to secure funding and build financial reserves, capital is increasingly flowing toward leading players, creating a significant “siphon effect.” Ji Kaiming, vice president of Winsoul Capital, told Caixin that some startups have seen their valuations jump from a few hundred million yuan to between 2 billion and 3 billion yuan in just two years.

Ji said follow-up funding will likely favor these top companies, as the robotics industry faces challenges such as a long capital cycle, uncertain technological pathways and unproven applications. “If the cycle spans three to five years, companies with more financial reserves will be better positioned to navigate future uncertainties,” he added.

Private market investors said robotics startups are already diverging into tiers based on valuation. Leading the pack are Galbot, Unitree, and AgiBot, each valued at more than $1 billion. A fundraising document viewed by Caixin showed that the two-year-old Unitree has raised more than $200 million and shipped several thousand units.

Ji highlighted a shift in robotics investment trends as early-stage funding has moved from hardware-focused firms like Unitree to specialized technologies. “Last year, motion control drove interest in ‘cerebellum’ technologies,” he said. “This year, large models for vision, motion and language have shifted focus to ‘brain’ technologies.”

With strong funding and policy support, robotics startups are rapidly expanding across China, as regions compete to attract emerging tech firms and drive economic transformation. This has spurred the growth of three major industry clusters in the northern Beijing-Tianjin-Hebei region, the eastern Yangtze River Delta, and the southern Pearl River Delta.

Xu Kun, a partner at China Renaissance Holdings Ltd., highlighted Beijing’s edge in foundational large model algorithms, thanks to its top universities. The Yangtze River Delta, including Shanghai and Hangzhou, offers a strong advanced manufacturing base, while the Pearl River Delta leverages its thriving mobile phone and automotive industries to build a robust robotics supply chain. This geographic diversity provides Chinese robotics companies with strategic flexibility and growth opportunities, said Xu.

As China’s governments increase support for AI and embodied intelligence, leading companies stand to benefit. In March 2025, embodied intelligence was named one of four future industries — alongside biomanufacturing, quantum technology and 6G — in the government work report.

Tech giants such as Huawei Technologies Co. Ltd. are entering the space, launching innovation centers and forming partnerships, while Tencent Holdings Ltd. is focusing on cloud and big data, aiming to collaborate with robotics manufacturers rather than compete in hardware.

Though big tech companies have yet to fully commit, their entry could be transformative. “Big tech will be the true variable in this sector,” said Ye Qian, president of Shoucheng Capital.

Tech breakthroughs

At the Spring Festival Gala, Unitree robots showcased precise control in complex maneuvers, highlighting the precise algorithmic control.

Shang Yangxing, CEO of BridgeDP Robotics, said the technical pathway for robotic motion control has become clearer and is advancing quickly. BridgeDP, a specialist in artificial cerebellum technologies that control robots’ movement, can program an untuned humanoid robot to walk within a week.

Shang noted that the standardization of hardware components such as joint modules and frames is simplifying robot building. However, effective interaction with the external world requires the integration of AI large models.

In February, Figure AI Inc., a U.S. company, unveiled Helix, a model capable of understanding language and motion, allowing robots to pick up any object. Chinese robotics companies are developing similar models. On March 10, Shanghai-based startup AgiBot launched its general AI model, the Genie Operator-1, designed to help humanoid robots understand human actions and perform real-world tasks.

However, training these models is made more challenging by a shortage of essential physical data. Although large language models benefit from extensive internet data, critical robotic AI data covering force and motion remains scarce, according to a Goldman Sachs report.

To tackle this data deficiency, AgiBot set up a data collection factory in Shanghai in 2024. The factory, now using around 100 robots, gathers 30,000 to 50,000 data points a day. By the end of the year, AgiBot had released the AgiBotWorld dataset, which includes more than 1 million trajectories from 217 tasks across five major scenarios. Despite this, AgiBot admitted the availability of high-quality, action-labeled data is still limited.

Innovation centers in Shanghai, Beijing and Shenzhen have stepped in to support startups with data needs. The Beijing Innovation Center has open-sourced Tiangang, a self-developed full-size robot platform, making it available to companies and research institutions. In addition, the industry’s first high-quality dataset, RoboMind, with 100,000 real-world data points from 279 tasks, was open sourced at the end of 2024.

Stepping into the real world

With rapid advancements in embodied intelligence hardware and software, many companies are pushing toward mass production and real-world applications, fueling expectations that 2025 will mark the pivotal year for humanoid robots to enter mass production.

In January, Tesla CEO Elon Musk announced the goal of manufacturing thousands of Optimus humanoid robots in 2025, with plans to increase production tenfold to 50,000-100,000 units in 2026, and further to 500,000-1 million by 2027.

In China, UBTech Robotics Inc. said it has secured orders for more than 500 humanoid robots from car companies, expecting to reach 1,000-2,000 orders by 2025. Meanwhile, AgiBot unveiled plans to produce more than 1,000 units and aims to expand sales to 3,000-5,000 by the end of 2025. Unitree’s humanoid robots have already surpassed 1,000 units in overseas sales.

The demand for mass production is closely linked to application deployment. Humanoid robots are beginning to find application in highly automated factory settings, such as automotive production lines, where they perform tasks such as assembling screws. Among the companies leading this movement, UBTech launched its industrial humanoid robot, Walker S1, in October 2024, deploying it for training in various companies, including Dongfeng Liuzhou Motor, BYD and Foxconn. Factories are favored for their semi-standardized environments, which present fewer distractions than home or commercial scenarios.

Robotics companies are focusing on enhancing the manual capabilities of these robots through factory training. For instance, SoHo Blink has introduced robots into Li Auto Inc. factories and logistics settings to refine their dexterity, gaining the necessary expertise to perform complex tasks, as real-world data from these environments is crucial for their development.

Despite advances, the cost of humanoid robots remains a barrier to replacing human labor. Currently, a single robot costs around 400,000 yuan and three are required to perform the equivalent work of one human, with a long payback period of seven years, according to Soochow Securities Co. Ltd. However, price reductions to 120,000 yuan per robot could allow a single robot to replace a human workstation, significantly reducing the payback period and enhancing the economic viability, the brokerage said in a research note.

Unitree and EngineAI have released robots for both industrial and consumer markets, priced between 88,000 and 99,000 yuan. UBTech’s latest offering, Tiangong Traveler, a life-size humanoid robot, is priced at 299,000 yuan and available for pre-order, targeting a broader range of application scenarios including retail sites.

Price plays a pivotal role in the consumer market. Digit, a developer of robots with human-like faces, currently sells its robots at 800,000 yuan, with the human-like face alone costing 200,000 yuan. The company is working on cutting costs by optimizing its supply chain, aiming to bring down the cost of a silicone face from 2,000 yuan to 200 yuan through mass production, which could potentially boost their annual revenue from millions to over a hundred million yuan, according to a company source.

Wei Dehao, CEO of Xingji Guangnian, a startup specializing in robotic dexterous hands, cautioned against rushing into price wars, suggesting that such strategies should wait until technology matures.

A multi-billion-dollar industry

The growing demand for the mass production of robots is boosting research and manufacturing investments in related upstream sectors, creating an industry chain which could be worth several hundred billion yuan.

For example, the market for actuators, vital components which convert energy into physical motion in Tesla’s humanoid robots, is poised for substantial growth. With each robot requiring 28 actuators each costing 3,000 yuan, producing 1 million robots would create a market worth 84 billion yuan, according to Soochow Securities estimates. Key Tesla suppliers such as Ningbo Tuopu Group, which has established a subsidiary in Mexico, are gearing up to meet this demand.

Domestic suppliers are also making strides in key components such as reducers, devices that allow robots to move joints and limbs with precision. The manufacture of these devices has been dominated by Japanese firms in the past. Chinese-made reducers are now replacing foreign counterparts, with the market share for Japanese harmonic reducers dropping slightly from 42.9% in 2021 to 41.6% in early 2024. For industrial robots, the share for Japanese RV reducers declined from 55% in 2022 to 44% in 2023, according to Orient Securities Co. Ltd.

According to Lu Juan, an analyst at CSC Financial Co. Ltd., the entry of Chinese suppliers has led to faster-than-expected cost reductions in the supply chain. Soochow Securities projected that the humanoid robot industry in 2025 will resemble the electric vehicle surge of 2014, signaling a decade of growth with the onset of domestic mass production.

Currently, domestic supply chain companies have not yet achieved large-scale revenue from humanoid robots, as many are still in the sample delivery phase. However, the technical barriers for humanoid robot suppliers are lower compared with industrial robots, aligning future profitability more closely with the automotive sector, said Lu.

“Success will depend on optimizing production processes and maintaining profitability despite competitive pricing,” Lu added.

This piece was originally published by Caixin Global. It is republished here with permission.

Reporters: Du Zhihang, Bao Hongyun, Liu Peilin, and Han Wei.

(Header image: A group of humanoid robots perform during the China Science Fiction Convention 2025 in Beijing, March 28, 2025. Zhang Kaixin/VCG)